Capitulation of the Bears…

First, before we go into the main news, you might want to go back and take a look at our 2023 Forecast piece back on January 3rd.

2023 Forecast – Eureka Perspectives (eureka-perspectives.com)

And I will just add mention of the dollar which we forecast back in January would head down to the 97.00 area this year. The recent low was 99.60, but that is not what we are here to talk about today. And we are not going to talk about the FED and how it seems determined to want to go into steep overkill mode with more rate hikes even though inflation is moderating. So, things are about to heat up with a lot of cross-currents.

What we are going to talk about today is Bloomberg’s resident expert, John Authers, who tonight, (Thursday 7/20) just came out with a piece suggesting that the market bears are about to capitulate Here is what he says:

“The year has barely passed its midpoint, and yet the market has barreled through most estimates for where Wall Street thought the S&P 500 would be at the end of the year. In the process, it defied the gloom accompanied by recession risks, soaring inflation and aggressive monetary tightening. And it’s left the strategists who made those estimates with a dilemma.

“It’s literally almost a strategist short squeeze,” Julian Emanuel of Evercore ISI told Bloomberg TV’s Jonathan Ferro on Tuesday, adding that his firm’s price target of 4,450 for the S&P 500 by the end of this year is one of the higher ones. It closed Thursday at 4,534.

That squeeze has forced strategist after strategist to revise their year-end call upwards, with Piper Sandler’s Michael Kantrowitz becoming the latest to do so on Thursday. The most bearish strategist in the poll conducted by Bloomberg’s Lu Wang in January, Kantrowitz raised his initial target of 3,225 to a range of between 3,600 and 3,800. Going with the lower end of the forecast, that implies a drop of as much as 20%, the most popular definition of a “bear market,” over the next five months.

He made clear that the move is solely a response to the market’s progress so far this year, and not to any change in Piper Sandler’s outlook toward US equities, which remains very bearish. It’s just that a fall of 29% from Thursday’s market close, implied by the previous target, now looks outlandish. “As we think about where the S&P 500 will end in 2023, the year-to-date move makes it difficult for us to continue justifying our year-end target that we published back in January as large-cap market indices have appreciated a lot year-to-date,” Kantrowitz wrote in a note to clients Thursday.

This fits a pattern in which a series of prominent strategists have had to revise upward their year-end calls — and done so in a way that seemed begrudging. Even now, the S&P 500 is just 6% shy of the highest current forecast (Fundstrat at 4,825), and a whopping 20% above the lowest one, from Piper Sandler.

T

New information has emerged over the last six months, and events have moved the market. They might well justify a higher year-end index value than seemed likely Jan. 1. And the move in the market itself is relevant. So there’s nothing necessarily shameful in a market strategist raising a target. To borrow the famous quote from Keynes, if the facts change then you should be prepared to change your opinion.

But now the complexity or what George Soros would call the “reflexivity” of the market takes a role. Markets can create their own reality. As the index rises, and influential investment houses raise their targets for it, so that adds to the momentum upwards in the share price. As in a short squeeze, the further the market rises, the harder it is for strategists to hold a line that is now looking increasingly bearish.

Taking the short squeeze analogy further, that means the strategists’ position is very bullish for the market. Eighteen of the two dozen houses covered by Bloomberg’s regular survey expect the S&P to decline between now and the end of the year. If and when they capitulate, that will add to the upward pressure on the market.

It’s also interesting that there’s still a wide variety of opinion over what exactly the bears got wrong. “What we failed to realize as a group in not being sufficiently bullish on the entire year is the effect of the extraordinary stimulus in 2020 and 2021 and the start of 2022,” said Emanuel of Evercore ISI. “Even if we have had historic tightening, it has not been enough to derail the economy.”

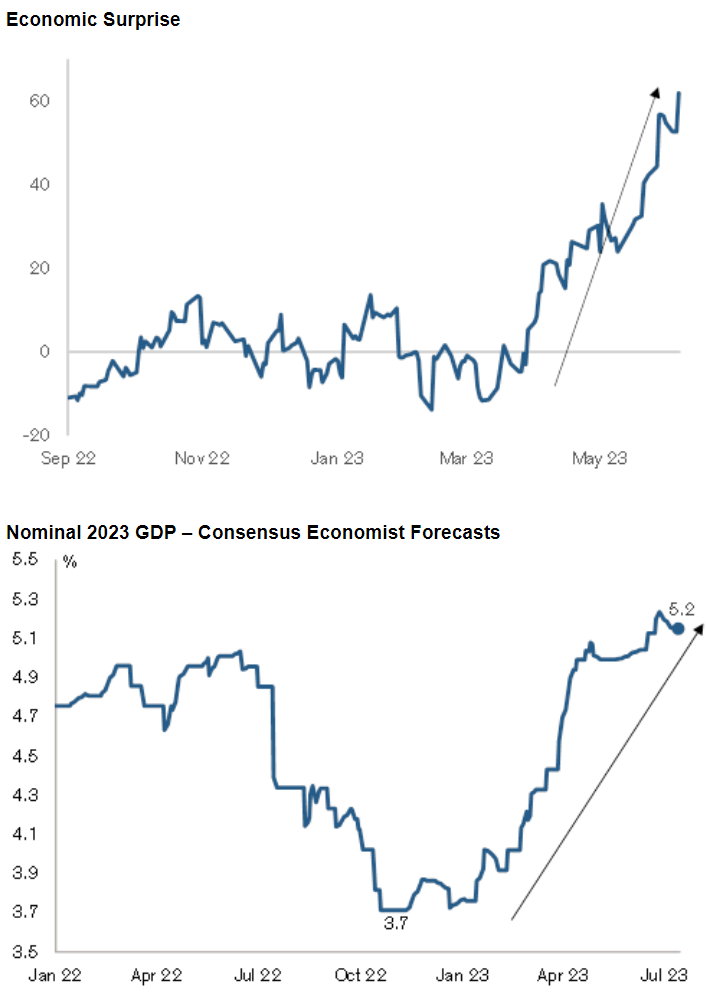

These charts from Credit Suisse illustrate this clearly enough. What were strategists to do when their economist colleagues were so far out?

|

Tom Hainlin, national investment strategist at US Bank Wealth Management, said that he had started to see what could almost be called an “economist capitulation.”

It’s the feared slowdown of the consumer that feeds into slowing corporate earnings that just hasn’t happened. And it’s been a fear for six months and 20 days coming into this year so far. So it’s the event that we’ve been concerned about that just hasn’t happened and people have had to revise their expectations of if it does, maybe it happens in the fourth quarter and maybe it’s more mild than we thought from the beginning of the year.

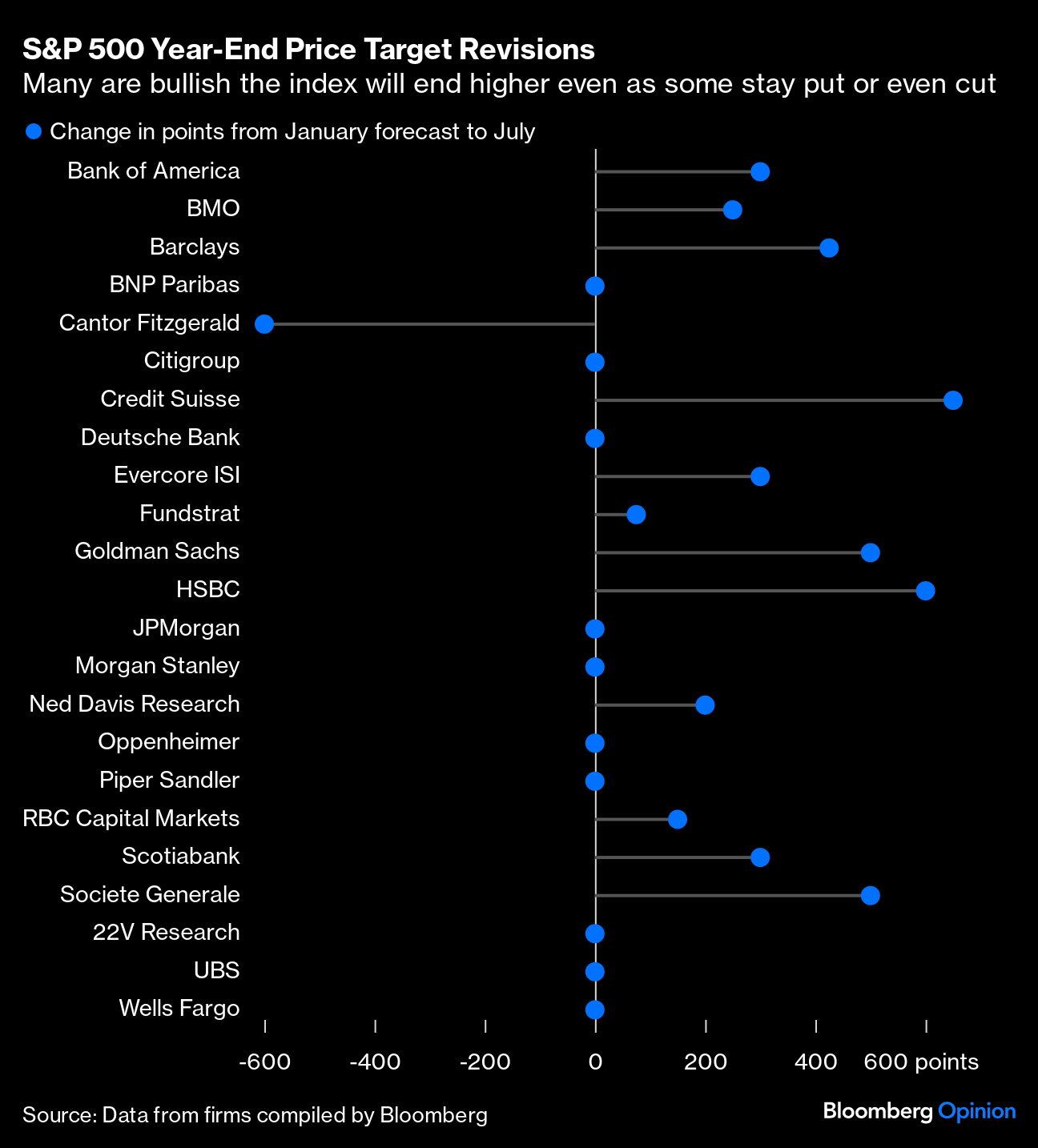

Bloomberg’s Wang meticulously records these changes of estimates. This is the latest table:

|

At the latest close, the S&P was ahead of the January year-end estimates for 22 of the 23 firms included in the poll. Fundstrat, then predicting a year-end 4,750, was the only exception. Perhaps even more remarkably, even after their upward revisions, all bar five of the houses in our survey expect the market to fall between now and Dec. 31. BMO, Credit Suisse, Fundstrat and 22V Research and HSBC are the only strategy groups currently calling for a rise. Many of them will be feeling pressure to raise their prices further. Looking at the magnitude of the changes in points terms, Credit Suisse’s Jonathan Golub has made the biggest adjustment so far, but several are close behind. The only firm we cover to cut estimates was Cantor Fitzgerald, which lowered its forecast around the time the banking crisis unfolded in March:

|

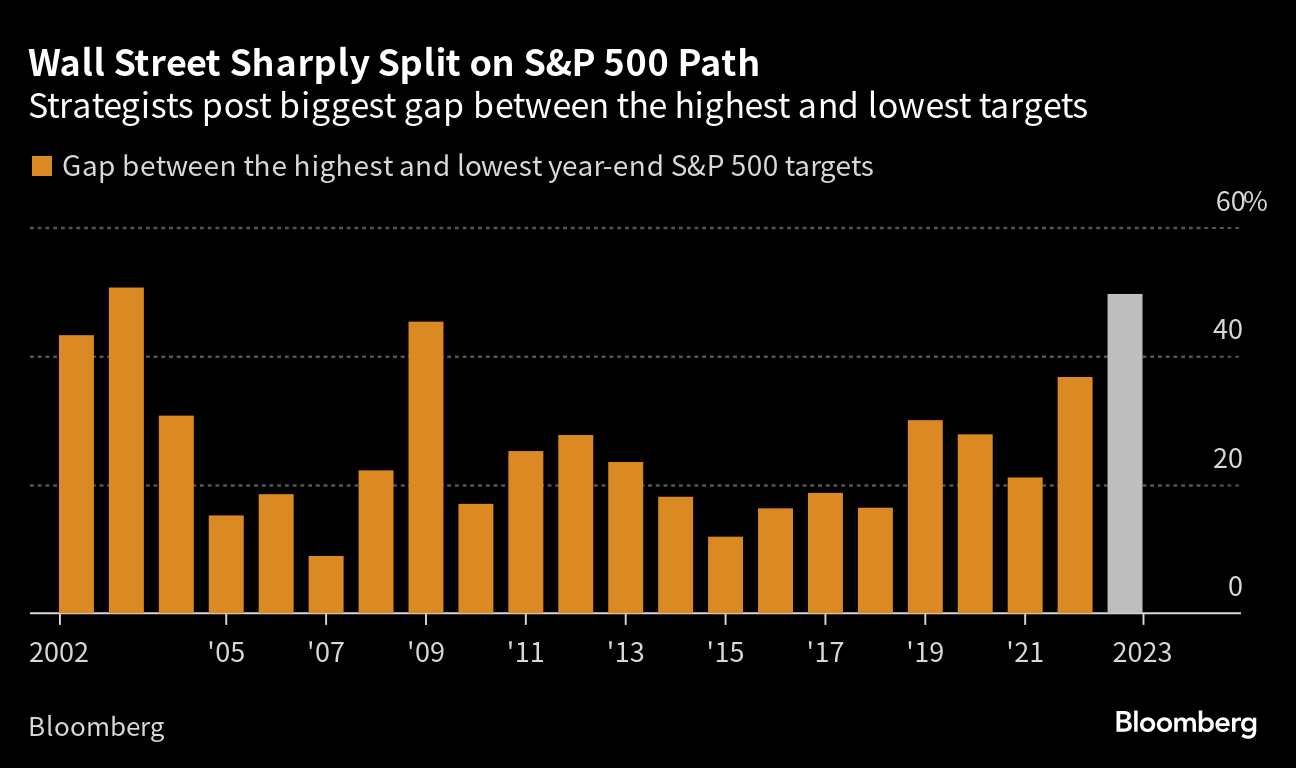

While the upward drift of estimates is obvious, the rally has also created even more division. As Bloomberg’s cross-asset team reported, there’s now a 30% difference between the most bullish call (Fundstrat) and the most bearish one (BNP Paribas).

|

The reasoning strategists offer for their changes is fascinating. Very few show any genuine enthusiasm. Lori Calvasina of RBC Capital Markets raised her estimate on the back of a lift in earnings forecasts and believes that the trailing price-to-earnings ratio of just over 20 is reasonable. That creates a risk the market could surge even higher:

This model, which is based on data going back to 1962, has been telling us for quite some time that consensus expectations for inflation, interest rates, and the economy in late 2023 imply a trailing P/E in the low 20s for the S&P 500. Using our revised S&P 500 EPS forecast for 2023 of $219, the 21.8x forecast P/E that the model produces today implies that the S&P 500 could end the year a bit higher from current levels in the 4,700 to 4,800 range. While that’s not our base case (we have other models that are far less constructive, and the combination of our bullish and bearish models has led us to a 4,250 target), it does keep us humble about the potential upside risks that exist for the S&P 500 through the end of the year.

When Manish Kabra of Societe Generale upped his bank’s target last month, he took pains to state that it was due to a “mania”:

There has been strong storytelling, and momentum mania, with ‘AI boom’ stocks adding 500 points to the S&P. We believe the AI momentum will build further in the second half and the 500-point rise will stay with us.

Despite this, he is still calling for the index to fall from here. Golub of Credit Suisse announced that his team was raising its 2023 S&P 500 price target to 4,700 (from 4,050 at the beginning of the year). That implies a gain of 3.6% from current levels with “modest upside from multiple expansion.” This is on a base case that “a recession will be averted, inflation will remain sticky near current levels, and monetary policy will tighten incrementally.” A rapid decline in inflation would move the index higher. As for the downside risks, Golub says: “Historically, elevated P/Es and depressed volatility have limited stock upside. Further, there are signs of a potential credit contraction, and economic weakness in China could hamper growth.”

Meanwhile, the few who saw a big rally coming are now suggesting more circumspection. Doug Peta of BCA Research avers that “the low-hanging equity fruit has already been picked now that the S&P 500 has risen 26% from its October lows” and that positive fundamental surprises will be harder to come by. However, he points out that momentum is favorable, and “the bears haven’t capitulated yet.” That’s fantastic for bulls, as it implies that the short squeeze on strategists can go on longer. “

With all that said, Authers really has not presented what the market has missed. All of you know what we have been pounding the table on for the past year, ever since the start of the technology growth curve, and that is the demand for technology to support the needs of the Climate Tech wave.

We will be releasing our forecast and discussion for the last half of the year after Powell’s news conference next week, probably Thursday evening.

Leave a Reply