It’s Over

All the FED posturing that we have been enduring since June 16, 2022 is over in my opinion. As of yesterday they have succeeded in puncturing the bubble, congratulations. Of course, if they had done their job correctly, we all could have avoided the chaos that evolved after August 2020.

Here are the reasons I say this:

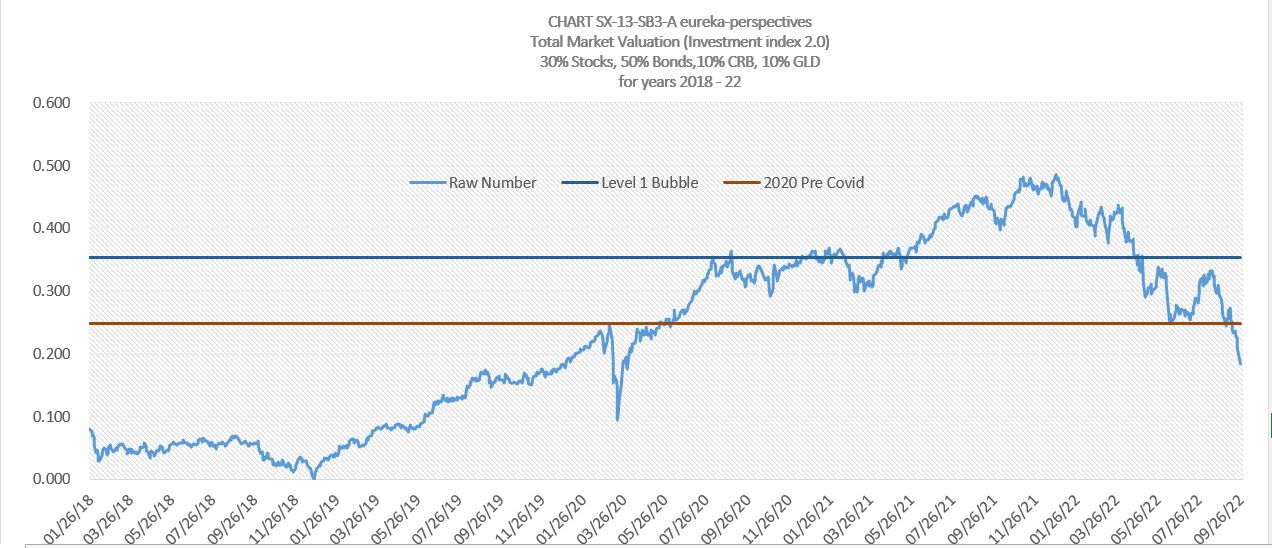

- As of yesterday the composite bubble of Bonds, commodities, stocks and gold has been punctured, regardless of how you calculate the start, somewhere between 3/30/20 and 11/4/20, my favorite point being August 7, 2020. Here is the chart we keep. As the legend on the chart indicates, this chart beginning in January 2018) has an index of market prices made up of 50% bonds, 30 % stocks, 10 % commodities, and 10 % gold. This makeup is based on a little research on what the total makeup of the market economy includes. The level 1 bubble line is based on August 7, 2020 values, while the 2020 Pre-covid line is the value before the COVID crash. You can see that the level 1 line supported the market a number of times between 6/17/22 and 9/6/22, leading me to believe that the bubble may not be punctured. But it now has happened as everything unraveled at the same time, stocks, bonds, commodities, and gold. At the lows S&P down 24 %, Nasdaq 100 down 33 %, 30 Yr Bonds down 39 %, CRB commodities down 20 %, and gold down 21 %.

2. The second reason is that the dollar has reached our long-term objective as outlined in yesterday’s post.

It is unfortunate that the FED actions now have a lot of investors short (based on data published the past few days). I don’t expect the FED to pivot and cut rates, but I do believe that as the lower input prices move into the supply stream, we will start to see the lower costs passed through to the consumer. Up until now the companies providing product to the consumer have been able to pass through their higher input costs and thereby maintain their earnings.

Moving on to our story….the Eureka-Perspectives Climate Change Portfolio

Here is the daily performance update for today, as we have promised. As before, the sectors shown in gold are the four sectors in the Climate Change portfolio with the EPCC designation being the composite of those four sectors. These performance numbers are for the period 6/6/22 (what we call the inflation high) and today’s close 9/26/22. We have shown the individual stock details of these four climate change sectors in past blogs, will try to list again later tomorrow.

To me what is important is that we have held our equity together during this period of FED chaos which has decimated so much of the economy.

Over the past three years with our macro S&P model we had a major dose of shorting stocks and continually increasing short positions through the August 2020-Janaury 2022 time period. While in the end we saw decent profits in terms of a reward/risk ratio I like the feel of being on the positive side of the economy for the coming round.

Sector % Return 6/6/22 to 9/26/22

Leave a Reply